How to Execute Customer Retention for Financial Services

Averi Academy

Averi Team

8 minutes

In This Article

AI-driven strategies to reduce churn: segment customers, map journeys, automate outreach, balance human contact.

Updated:

Trusted by 1,000+ teams

Startups use Averi to build

content engines that rank.

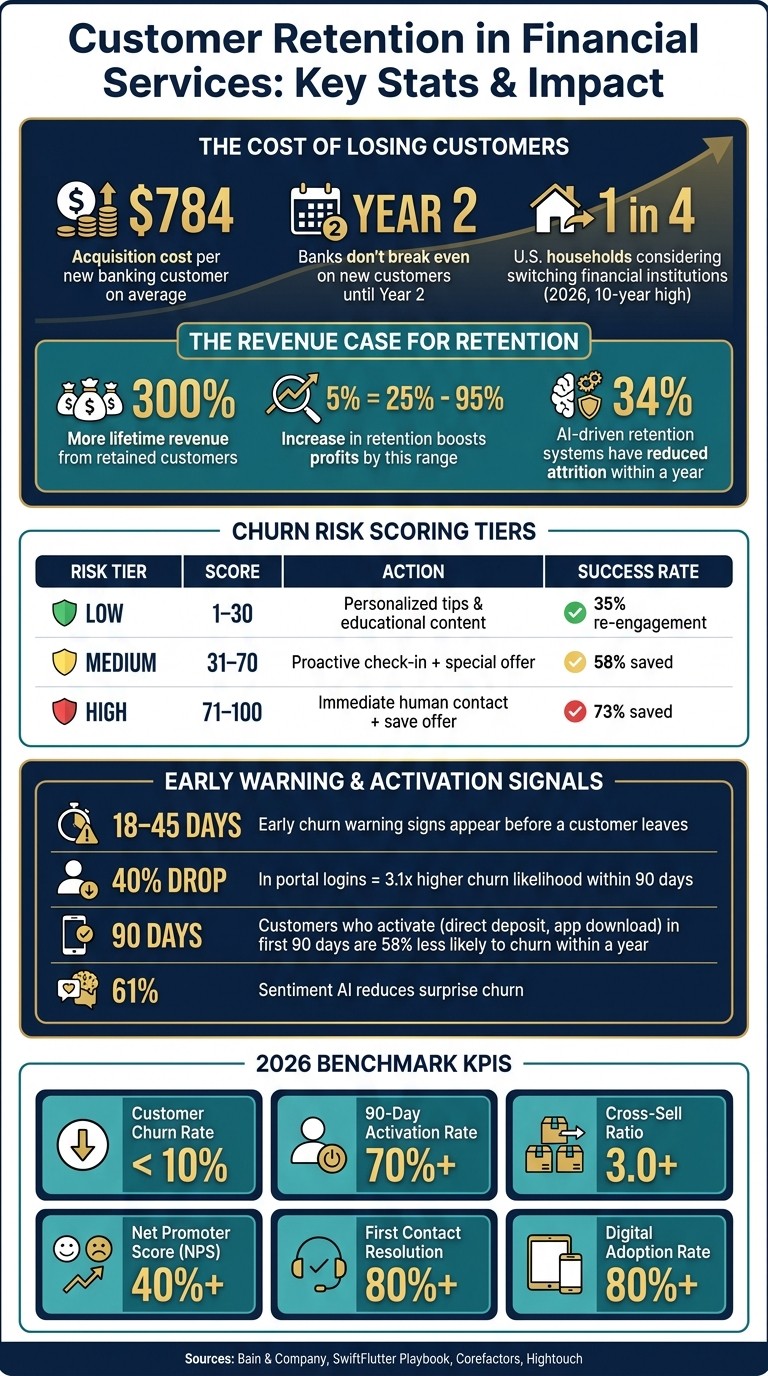

In financial services, retaining customers is far less expensive than acquiring new ones. On average, acquiring a new banking customer costs $784, and banks typically don’t break even until the second year. Retained customers generate up to 300% more revenue over their lifetime, and even a 5% increase in retention can boost profits by 25% to 95%. Yet, in 2026, customer switching in U.S. banking has reached a 10-year high, with 1 in 4 households considering switching financial institutions.

The article outlines key strategies for improving customer retention, including:

Using AI and automation to predict churn and deliver personalized outreach.

Segmenting customers by behavior to tailor retention efforts effectively.

Mapping the customer journey to identify and address critical drop-off points.

Tracking engagement metrics like login frequency and activation rates.

Balancing automation with human contact for high-risk or high-value customers.

Designing trust-building loyalty programs that go beyond transactional incentives.

Customer Retention in Financial Services: Key Stats & Impact

Building the Foundation of Your Retention Strategy

Retention strategies thrive on clarity: before automating workflows, you need to define the problem, identify your target customer segments, and establish the metrics that matter. With these foundational steps in place, you can effectively measure and refine your retention efforts.

Setting Retention Goals and KPIs

Vague goals won’t cut it. Set specific, measurable targets - like cutting churn from 21% to 16% over the next year or increasing high-value Customer Lifetime Value. Start by establishing a baseline using metrics such as churn rate, CAC payback, NPS, and First-Contact Resolution. Complement these with additional KPIs like CSAT, Average Handle Time, and cross-sell conversion rates to get a comprehensive view of retention health. For example, banks that leverage advanced analytics to predict churn have achieved a 15% to 20% improvement in customer retention[2]. This demonstrates how pairing clear goals with actionable data can drive tangible results.

Segmenting Customers for Targeted Retention

Not all customers are the same - treating them uniformly risks alienating your most valuable ones. Effective segmentation goes beyond basic demographics like age or income and instead focuses on behavioral patterns. This means analyzing how customers use your products, how often they engage, and what their financial behaviors signal.

For example:

The Disengaged Depositor: Maintains a high account balance but uses only one product.

The Intent Rich Explorer: Frequently visits loan calculators or savings tools without converting.

Each of these profiles requires a tailored retention approach. Implement a risk-based churn scoring system (using a 1–100 scale) to prioritize responses:

Risk Tier | Score | Automated Action | Success Rate |

|---|---|---|---|

Low | 1–30 | Personalized tips and educational content | 35% re-engagement |

Medium | 31–70 | Proactive check-in + special offer | 58% saved |

High | 71–100 | Immediate human contact + save offer | 73% saved |

Source: SwiftFlutter Playbook [9]

The first 90 days of a customer’s journey are particularly critical. Customers who complete key activation steps - like setting up direct deposit or downloading the app - during this period are 58% less likely to churn within a year[7]. Using AI to automate engagement tailored to these segments ensures you scale personalized outreach effectively.

Once segmentation is in place, your next step is to align follow-up actions with each group’s specific behaviors.

Setting Up Data-Driven Follow-Up Systems

The best retention systems don’t wait for customers to complain - they proactively identify friction points. Early warning signs, like reduced logins, lower transaction volumes, or frequent visits to help pages, can appear 18 to 45 days before a customer decides to leave[7]. Start by mapping your current retention process to uncover delays or manual bottlenecks, and define the trigger events that should prompt action.

For instance, if a customer spends over 40 seconds on a loan application page without completing it, this could trigger a contextual chatbot nudge or a callback offer. However, for more sensitive situations, ensure these cases are escalated to human agents - automation has its limits, especially when trust is at stake.

"Retention starts long before someone looks 'at risk.' If a customer never reaches value, gets stuck early, or doesn't build a habit, churn is usually a matter of time." - Team Braze[10]

Mapping the Customer Journey to Find Key Retention Moments

Every stage of the customer journey holds a different level of influence over whether a customer decides to stay or leave. Identifying these moments and having a well-thought-out plan can transform retention efforts from reactive to proactive. These ideas build on earlier discussions about using data to drive retention strategies and pave the way for creating customized outreach workflows.

Key Retention Stages in Financial Services

In financial services, the customer journey typically unfolds across six stages: acquisition, activation, engagement, retention, loyalty, and advocacy. Each stage comes with its own set of challenges and opportunities.

Stage | Customer's Core Question | Strategic Focus |

|---|---|---|

Acquisition | Do I trust this provider? | Frictionless onboarding, precision targeting [2] |

Activation | Is this worth my time? | Deliver a "moment of truth" in the first 3 touchpoints [2] |

Engagement | Are you solving my problem? | Personalize using behavioral insights [2] |

Retention | Why should I stay? | Proactively address drop-off triggers via predictive AI [2] |

Loyalty | Do you reflect my values? | Build emotional affinity via tailored programs [2] |

Advocacy | Would I tell others? | Amplify referrals and testimonials [2] |

The activation stage is particularly critical. Providing a meaningful experience within the first three interactions - such as offering a credit snapshot or a savings projection - can reduce churn by over 30% within the first 30 days [2]. Beyond activation, certain events like policy renewals, loan expirations, or investment anniversaries become high-risk moments when customers are more likely to explore competitors [3][1]. Understanding these stages is key to spotting disengagement cues and delivering timely, effective responses.

Spotting the Warning Signs of Disengagement

Churn often starts subtly, with gradual declines in engagement.

"The most dangerous churn is invisible. It's the slow fading of engagement, trust, and perceived relevance." - Corefactors [2]

AI tools can detect these early signs, such as a 40% drop in portal logins over 30 days, which correlates with a 3.1x higher likelihood of churn within 90 days [12]. Sentiment analysis tools, using NLP, can flag frustrated tones in customer chats and support interactions, cutting "surprise" churn by 61% [12].

Life events like job changes or home purchases also act as churn triggers. By analyzing CRM data and public records, AI can alert relationship managers to these transitions, enabling proactive outreach.

Balancing Automation with Human Outreach

When warning signs appear, deciding whether to use automation or human intervention becomes crucial.

"The result is a smarter retention engine: always-on, adaptive, and personalized at scale, with AI delivering intelligence and automation, and humans bringing context and empathy." - Craig Dennis, Hightouch [13]

AI is well-suited for managing routine tasks like onboarding, low-risk re-engagement, and nudges. However, high-value customers showing signs of disengagement or facing sensitive issues often need the personal touch. For example, if a high-LTV customer lingers on a loan eligibility page for over 40 seconds while also showing declining activity, this should trigger an immediate callback from a human representative.

"Retention must be designed around 'trust moments,' those high-stakes interactions where expectations and communication must align perfectly." - N Suresh, Corefactors [2]

To avoid over-messaging, it’s also crucial to set limits on email, SMS, and push notifications. Over-communicating can unintentionally push customers further away, emphasizing activity metrics over genuine relationship health.

Building Personalized Outreach Workflows

To advance AI-powered retention strategies in financial services, the next logical step is creating dynamic outreach workflows that deliver tailored, automated responses. Once you've pinpointed disengagement signals and identified the critical moments when customers are likely to leave, it's time to implement workflows that ensure consistent, personalized communication. These workflows, grounded in data-driven insights, can significantly strengthen your retention efforts.

Creating AI-Powered Communication Workflows

Instead of sticking to rigid, calendar-based schedules, develop workflows that respond dynamically to customer behavior. AI systems can monitor specific events - like stalled direct deposits, reduced login activity, or incomplete loan applications - and trigger targeted responses via email, SMS, in-app notifications, or advisor callbacks. This eliminates the need for manual intervention while ensuring timely outreach.

To build such workflows, follow these steps:

Define a clear objective, such as reducing churn.

Map out the current manual processes.

Identify behavioral triggers that can replace static timing.

Configure AI agents with business rules tailored to the financial sector.

By automating routine tasks, you free up your team to focus on more impactful, human-centered interactions.

Take this example: In 2025, Rachel Okonkwo, Chief Revenue Officer of a $38M digital lending fintech serving 65,000 borrowers, revamped her company's retention strategy by focusing on the 60-day activation window. Instead of relying on late-stage win-back campaigns, she implemented an AI-driven engagement sequence. The result? A 28% drop in 90-day churn within six months, preserving approximately $2.1M in annualized revenue [7].

Personalizing Message Timing and Channel

Using insights from behavioral segmentation, you can fine-tune both the timing and delivery method of your outreach to maximize its effectiveness. Move beyond basic demographic segmentation and focus on customer intent and financial behavior.

"Retention isn't saved in strategy decks - it's saved in seconds." - Corefactors [2]

For instance, a customer who spends over 40 seconds on a loan eligibility page is signaling high intent. This scenario calls for an immediate, contextually relevant response - not a delayed follow-up email [2]. On the other hand, a customer showing gradual signs of disengagement may need intervention 18 to 45 days before they decide to leave [1][7]. A tiered approach works well here: low-risk customers can receive automated, personalized content, while high-risk, high-value customers should trigger escalation to a human advisor [1].

Managing Compliance in Regulated Communications

In financial services, automation must operate within strict regulatory frameworks, necessitating human oversight at critical points. For communications involving sensitive financial transactions, include mandatory approval steps before messages are sent [10].

Set clear escalation rules for automated and human-initiated communications, and implement validation checks to catch errors - such as promotional offers that haven’t been reviewed against current disclosure standards [5]. Additionally, maintaining a detailed audit trail for every automated message - including its trigger, content, and timing - helps protect your organization and ensures compliance.

Loyalty Programs and Value Expansion

Designing Retention Offers That Build Trust

Basic cashback deals and points systems often fall short when it comes to fostering genuine loyalty in financial services. As Corefactors aptly states: "Loyalty is not a program, it's a response... it's a by-product of consistent emotional resonance and not just transactional incentives." [2] The most impactful retention strategies focus on the overall customer relationship rather than isolated transactions.

One effective approach is relationship-based pricing, which rewards customers for consolidating their financial activities. For example, customers who maintain a checking account, savings account, and a loan with the same institution might receive benefits such as a 0.25% reduction on mortgage rates or waived fees. Tiered loyalty programs, like Silver, Gold, and Platinum levels, work well when the criteria are clear and the benefits resonate with customers, offering both financial perks and an emotional connection.

American Express exemplifies this concept by building its retention strategy around identity rather than just competitive rates. By associating its cards with exclusive travel perks, elite recognition, and global privileges, Amex creates a sense of belonging that makes switching banks both emotionally and financially unappealing. [2]

Using Cross-Sell and Upsell Strategies Effectively

Once trust is established through personalized offers, the next step is to identify moments when customers are most likely to engage with additional products. Major life transitions often present these opportunities. For example, when a customer’s direct deposit increases, they start exploring home equity options, or their child approaches college age, these moments are ideal for offering relevant products.

AI-driven next-best-action models excel in identifying these opportunities by analyzing real-time customer data. These tools can generate up to three times the return compared to broad, untargeted campaigns. [1] Personalization engines, which use this data to tailor recommendations, have been shown to deliver a 10% to 15% increase in revenue for financial institutions. [2] The goal is to align product recommendations with actual customer needs, avoiding the temptation to push products that may undermine trust for short-term gains.

"Banks need to understand that inertia isn't loyalty. Most customers stay because it's harder to change banks, not because they love their bank." - Kristin McCauley, President, Mills Marketing [14]

Tracking Product Adoption to Increase Engagement

Selling a product is only the first step in building a lasting customer relationship. The real challenge lies in ensuring customers actively use the products they’ve signed up for. Sustained engagement is a critical predictor of long-term retention.

Tracking how customers use specific features - such as setting up autopay, utilizing budgeting tools, or linking external accounts - provides valuable insights. A decline in feature usage can be an early warning sign of churn, often occurring 18 to 45 days before a customer decides to leave. [7] For high-value customers, a drop in engagement with key features should prompt targeted re-engagement efforts rather than generic outreach.

Customers who view their bank as their primary financial provider are twice as likely to purchase additional products and three to four times more likely to consider future offerings. [6] In this way, product adoption isn’t just an engagement metric - it’s a direct driver of revenue growth. Leveraging tools like Averi’s AI-powered workflows can help banks maintain continuous, personalized engagement, ensuring customers stay connected and invested in their financial relationship.

Measuring and Improving Retention Over Time

Key Metrics to Track

Tracking the right metrics is essential for understanding and improving customer retention. Instead of focusing solely on lagging indicators like churn confirmation, it's more effective to monitor leading signals that help predict and prevent customer loss. While the average annual churn rate in banking ranges from 12% to 15%, top-tier institutions manage to keep it under 10% [1].

Here’s a breakdown of metrics that provide a comprehensive view of retention health:

Metric | What It Measures | 2026 Benchmark Target |

|---|---|---|

Customer Churn Rate | Percentage of customers who leave annually | Below 10% |

90-Day Activation Rate | New customers fully activated within 90 days | 70%+ |

Cross-Sell Ratio | Average number of products per customer | 3.0+ products per household |

Customer Effort Score (CES) | Ease of accomplishing goals (1–5 scale) | Below 2.0 |

Net Promoter Score (NPS) | Willingness to recommend | 40+ |

First Contact Resolution | Service issues resolved on first interaction | 80%+ |

Digital Adoption Rate | Customers actively using digital channels | 80%+ |

The 90-day activation rate is a critical focus. Customers who fail to establish direct deposits or fully activate their accounts within this period are much more likely to churn [1]. Identifying and addressing this early is where predictive systems can make a real difference.

Using Feedback and Service Data to Find Pain Points

Churn often happens quietly. Customers rarely voice their dissatisfaction before leaving - they simply disengage. This makes it vital to monitor behavioral signals in service data rather than waiting for explicit feedback.

Key indicators include a drop in login frequency (even a 40% decline can signal elevated churn risk), unresolved support tickets, or repetitive issues raised through customer service channels. Additionally, tools like natural language processing can analyze support interactions and emails to detect sentiment changes before they escalate.

"Sentiment AI turns subjective relationship intuition into a structured, auditable, and actionable data layer that scales across every client relationship regardless of advisor bandwidth." - Arete Intelligence Lab [12]

The value of these insights is evident. In 2025, Marcus Henley, a Managing Principal at an independent RIA with $310M in assets under management (AUM), introduced predictive churn alerts and workflows to detect life events. By Q3 2025, his firm reduced its annualized attrition rate from 9.1% to 5.6%, retaining approximately $18M in AUM that would have otherwise been lost [12]. Notably, 61% of high-net-worth clients who left advisory firms cited a lack of proactive communication as the main reason [12]. Consistent sentiment monitoring has been shown to reduce unexpected client departures by the same percentage [12].

Refining Workflows Based on Performance Data

Collecting data is only the first step. The real challenge lies in using that data to refine retention workflows and strategies.

AI-driven churn models typically achieve prediction accuracies of 85% to 95%, significantly outperforming traditional rule-based systems, which average around 72% [6][11]. However, these models require regular updates to stay effective. Retraining them every 24–36 months ensures they remain accurate [11]. Combining this with A/B testing - experimenting with different message tones, call-to-action styles, and delivery channels - can help fine-tune engagement strategies.

A tiered response system offers a practical way to act on churn predictions. Assign customers a churn risk score (Low, Medium, or High) and tailor responses accordingly. For instance:

Low-risk customers: Automated reminders or nudges.

High-risk, high-value customers: Direct outreach from a relationship manager.

Organizations that use these AI-powered interventions have reduced preventable churn by 40% to 60% within 90 days [9].

"Insight ≠ Action & Prediction ≠ Conversion. These legacy stacks might predict churn, but they can't prevent it." - FCI-CCM [4]

The secret to success lies in closing the loop. Performance data should directly inform workflow adjustments, ensuring insights lead to timely actions. Review new workflows after the first week of implementation, followed by monthly evaluations to refine the approach further [5][8]. This iterative process ensures your retention strategy stays aligned with evolving customer behaviors.

Conclusion: Building a Retention Model That Lasts

Customer retention in financial services isn’t just a project with a start and end date - it’s a system that needs constant attention. The companies that succeed over the long haul aren’t waiting until customers leave to react; they’re building frameworks designed to prevent churn before it happens.

As discussed earlier, moving toward a unified, data-driven approach is essential. By using AI and real-time data, firms can shift from reactive tactics to proactive strategies. This involves maintaining clean customer data to fuel accurate AI insights, using behavioral triggers to time outreach perfectly, and ensuring human advisors step in when empathy is crucial. Fred Reichheld of Bain & Company emphasizes the power of retention:

"Improving customer retention by just 5% can boost profits by 25%, and in some cases, up to 95%." [4]

The stakes are high. With U.S. banking switching behavior at a 10-year peak - 1 in 4 households now considering switching their primary financial institution [1] - a passive approach to retention is more costly than ever. Firms that have embraced AI-driven retention systems have already seen attrition rates drop by up to 34% within a year [12]. That’s not just an improvement - it’s a competitive edge.

The way forward isn’t about piling on more tools; it’s about connecting the dots between data, action, and learning. Start small. Take one workflow, like onboarding, and ensure it runs smoothly. Measure its impact, refine it, and then expand. Each new workflow, feedback loop, and tested action makes the system smarter and more effective over time.

"Retention is no longer a marketing metric - it's a bank growth lever." - Harsh Pranav, FCI-CCM [4]

The firms that approach retention as a core infrastructure, rather than a one-off campaign, are the ones building relationships that grow in value over time. The tools and technology are already in place - what matters now is your organization’s commitment to making it happen. This model brings together the actionable, AI-driven strategies discussed earlier, setting the foundation for long-term success.

FAQs

What data is needed to predict churn in a bank or fintech?

To anticipate customer churn in a bank or fintech setting, focus on collecting data that reveals behavior, satisfaction, and engagement patterns. This includes details like transaction history, frequency of logins, customer feedback, onboarding experiences, service usage stats, and complaint records. Additionally, keep an eye on external influences such as market trends or competitive offers. By analyzing this information, you can create predictive models to pinpoint customers who may leave and take steps to retain them.

How do I know when to use automation vs. a human advisor?

To handle tasks effectively, leverage automation for repetitive, data-focused activities such as predictive analytics, chatbot interactions, or automated outreach. This approach allows you to scale personalized experiences with greater efficiency. Meanwhile, assign human advisors to more nuanced, high-touch responsibilities that demand empathy, critical thinking, or tailored guidance - like onboarding new clients or addressing sensitive concerns. By blending these approaches, you can streamline operations while prioritizing trust and meaningful relationship-building during pivotal moments.

How can I launch a retention workflow in 30 days?

To get a customer retention workflow up and running in just 30 days, begin by mapping out your customer journey to pinpoint critical moments where AI can help predict churn and tailor interactions. Leverage tools such as predictive analytics or chatbots to identify clients who may be at risk and automate personalized outreach. Platforms like Averi AI can streamline workflow management, ensuring smooth execution. Lastly, track customer feedback and engagement metrics, making adjustments as needed to refine your approach within the 30-day timeline.

Related Blog Posts

Zach Chmael

CMO, Averi

"We built Averi around the exact workflow we've used to scale our web traffic over 6000% in the last 6 months."

Your content should be working harder.

Averi's content engine builds Google entity authority, drives AI citations, and scales your visibility so you can get more customers.